2025 HECM Limit Rises to $1,209,750: Expanded Access for Homeowners with Higher-Value Properties

Mike Branson Jr. – Author

Mike Branson Jr. has 25 years of experience in the mortgage banking industry. He has devoted the past 19 years to reverse mortgages exclusively. Mike has worked in several aspects of the Mortgage industry, including Loan Origination, Underwriting, and Management.

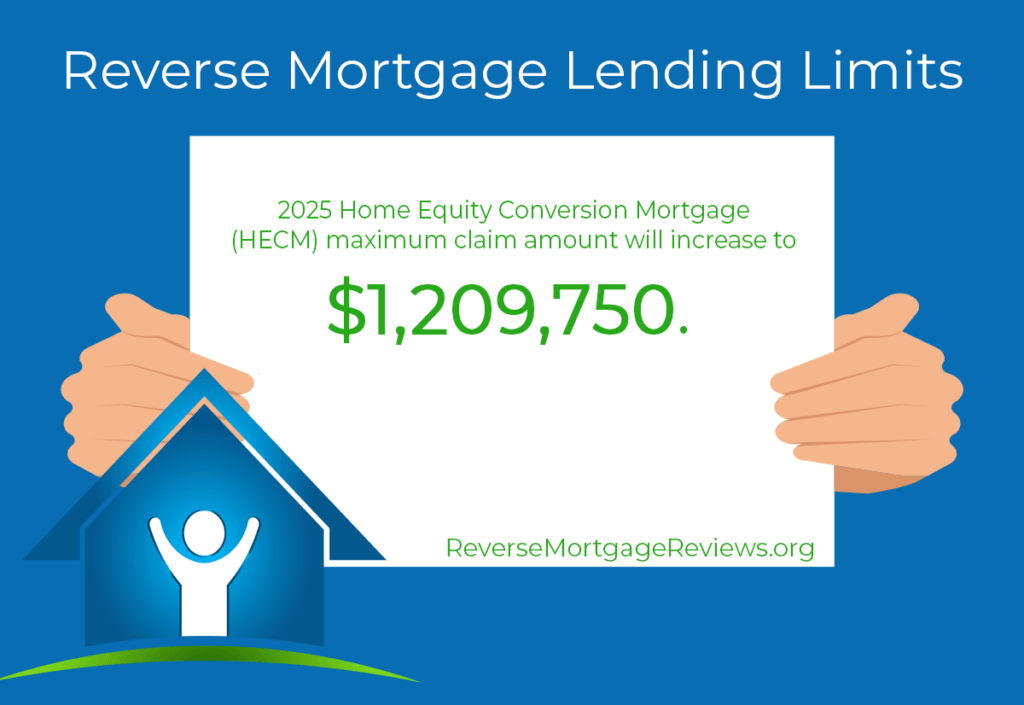

In a major move benefiting older homeowners nationwide, the Federal Housing Administration (FHA) has announced that the 2025 Home Equity Conversion Mortgage (HECM) maximum claim amount will increase to $1,209,750. This new limit takes effect for case numbers assigned on or after January 1, 2025, replacing the 2024 cap of $1,149,825.

This adjustment, detailed in Mortgagee Letter 2024-21, applies to all 50 states and U.S. territories, including Alaska, Hawaii, Guam, and the Virgin Islands. The change will also be reflected in HUD?s Single Family Housing Policy Handbook 4000.1.

Greater Flexibility for Homeowners in High-Value Markets

This latest increase is particularly meaningful for homeowners with higher-valued properties. Reverse mortgages?especially the federally insured HECM program?allow older homeowners to convert part of their home equity into cash without monthly mortgage payments.

With the new 2025 limit, borrowers can access more of their home?s value than ever before, giving them greater flexibility to manage expenses, fund home improvements, or bolster retirement income.

Understanding the HECM Reverse Mortgage

A reverse mortgage is a loan designed for homeowners aged 62 or older that allows them to withdraw a portion of their home equity while continuing to own and live in the property. The loan doesn?t have to be repaid until the borrower sells the home, moves out, or passes away.

The HECM, insured by the FHA, remains the most popular and secure reverse mortgage option available, with built-in protections for both borrowers and heirs.

What the 2025 Limit Increase Means

-

Larger Loan Amounts: Borrowers can now qualify for higher proceeds, especially those with homes valued near or above $1 million.

-

Competitive Alternative to Jumbo Reverse Mortgages: With a higher FHA-insured cap, some homeowners may no longer need a private jumbo reverse mortgage. The HECM?s federal insurance and non-recourse protections often make it a safer choice.

-

Reflects Rising Home Prices: HUD?s annual adjustment mirrors continued growth in U.S. home values, ensuring that the HECM program keeps pace with today?s housing market.

Historical Perspective and Future Outlook

Over the past 15 years, the HECM lending limit has steadily risen?from $625,500 in 2009 to $1,209,750 in 2025?reflecting HUD?s responsiveness to market trends. These annual increases help preserve the program?s relevance amid changing home prices and economic conditions.

Looking ahead, future adjustments will likely continue in response to inflation, housing demand, and broader financial trends that shape retirement planning for older Americans.

Expert Guidance for Homeowners

While the higher limit opens new opportunities, it?s important for borrowers to understand how age, interest rates, and home value affect loan proceeds. Speaking with a HUD-approved lender ensures personalized guidance based on your financial goals and eligibility.

5 Key FAQs About the 2025 HECM Limit

1. What is the new 2025 HECM limit?

The new maximum claim amount is $1,209,750, effective January 1, 2025. This allows eligible borrowers to access more of their home equity.

2. How does this affect my available loan proceeds?

A higher FHA limit means borrowers with high-value homes may now qualify for larger reverse mortgage payouts.

3. Is refinancing an older reverse mortgage worth it in 2025?

If your home value or the lending limit has increased significantly, a HECM-to-HECM refinance could unlock more equity?subject to HUD?s 5x benefit test and new principal limit factors.

4. How is the HECM lending limit determined?

HUD bases the annual HECM limit on 150% of the national conforming loan limit set by Freddie Mac.

5. What determines my personal loan amount?

Key factors include your age, current interest rate, and the lesser of your home value or the HUD limit.

Summary

The 2025 increase in the HECM lending limit to $1,209,750 marks another milestone in the evolution of the reverse mortgage program. It?s a positive development for homeowners in higher-value markets, providing greater access to equity, financial flexibility, and federally insured protection.

If you?re considering a reverse mortgage or refinance, take a few minutes to see what you could qualify for with our reverse mortgage calculator?no personal information required.

|

No Comments on “2025 HECM Limit Rises to $1,209,750: Expanded Access for Homeowners with Higher-Value Properties”

|