HECM vs HELOC Loan Comparison: Which is Best for You?

Mike Branson Jr. – Author

Mike Branson Jr. has 25 years of experience in the mortgage banking industry. He has devoted the past 19 years to reverse mortgages exclusively. Mike has worked in several aspects of the Mortgage industry, including Loan Origination, Underwriting, and Management.Although the costs to establish a HELOC (Home Equity Line of Credit) with a HECM (Home Equity Conversion Mortgage) are higher and you do have mortgage insurance premium (MIP) on the loan as well that does add an additional .50% to the accrual (the MIP is not interest but it accrues the same way), the interest rates for a HECM line of credit are very comparable to a Home Equity Line of Credit you would receive from a bank.

Let's talk about the differences because they are immense

We talked about the cost to set it up. The HELOC from your local bank would almost certainly be less to set up so that is in its favor. But after that, the reverse mortgage line of credit has a lot going for it that the HELOC does not.

HELOC loans are harder to qualify

A HELOC has a much more stringent qualification criteria which many retired borrowers no longer meet.

Time was when all you had to have was equity in your home to qualify for a HELOC but too many people found themselves in debt with no reasonable expectation of being able to make the required payments and therefore, laws were passed that require lenders to meet "ability to repay" rules that are more stringent than a reverse mortgage that requires no monthly payments (but there are some underwriting requirements as you must be able to demonstrate that you can at the least pay all property charges such as taxes and insurance as well as have a minimum amount of residual income remaining on which to live).

HELOC loans require monthly payments and recast after 10-years

The HELOC requires the borrower to make payments, usually of interest only, during the draw period and then the loan enters a repayment period.

This means that borrowers can go 10 years at lower payments on which the balance is not declining on the loan unless they pay more than the minimum payment due and then the loan recasts to a payment amount that will repay the obligation in full in the remaining term ? usually 20 years.

Payments can go up as much as 2 to 3 times what the borrower was paying.

HECM loans require no monthly payments

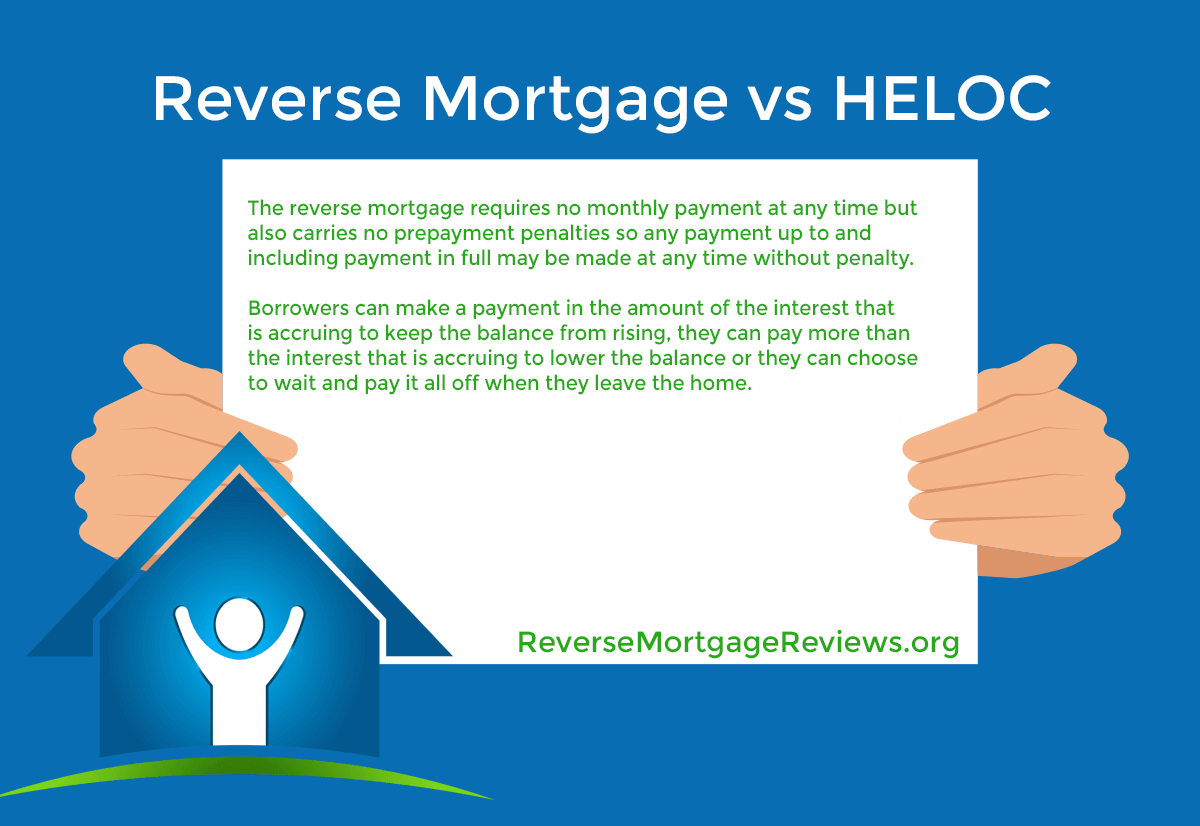

The reverse mortgage requires no monthly payment at any time but also carries no prepayment penalties so any payment up to and including payment in full may be made at any time without penalty.

Borrowers can make a payment in the amount of the interest that is accruing to keep the balance from rising, they can pay more than the interest that is accruing to lower the balance or they can choose to wait and pay it all off when they leave the home.

How much is left for the homeowner as you put it depends entirely upon how they choose to proceed. Borrowers can compare an amortization schedule for a standard or forward loan to that of a reverse mortgage and you will see that on a regular loan or on a HELOC, you also pay a lot of interest over the years and then you still have the principal left to pay.

The difference is not as great as you would believe because with the forward loan you are paying the monthly payments and on the reverse mortgage, if you paid them as well you would have just as much left but if you choose to pay nothing, you have the spendable (or savable) cash each month that you would not have otherwise had.

What you have left over in either circumstance depends on you and your spending needs. Obviously if you do not need any loan, you would most certainly have more equity left without a need to borrow.

HECM loans have a unique line of credit growth feature

Unlike a HELOC, a HECM grows over time on the unused balance. This is not interest anyone is paying you, it is an increase in the amount available to you.

If you have you line for many years and have not used it or all of it, the remaining balance available is growing giving you more access to funds later should you need them.

Also unlike a HELOC where the lender can cut or close the loan at any time without notice, the reverse mortgage cannot be closed or cut as long as you live in the home and abide by the terms of the loan (pay your taxes and insurance in a timely manner).

If you are making payments on a reverse mortgage and find that you cannot at times or must stop entirely, there are no adverse ramifications for doing so.

If you did that with a HELOC, you would injure your credit rating and risk foreclosure. The reverse mortgage changes since the Trump administration is that the rates are now low enough so that the new loans being written give borrower higher loan amounts now.

One of the factors that determines the amount of money a borrower will receive is the interest rate on the loan (in addition to the age of the youngest borrower on the loan, the property address and the HUD lending limit).

Since the pull back of the Principal Limit Factors, the market has been much more receptive to jumbo reverse mortgages or proprietary programs as well.

We have seen several new programs emerge in just the past few years allowing more borrowers access to more private programs and at better rates.

Summary

When researching a reverse mortgage, it's important to speak to your family and trusted financial advisor to weigh both the pros and cons.

Learn more about how a HECM loan might be right for you by contacting one of our top reverse mortgage lenders, or check your eligibility with our free reverse mortgage calculator.

|

No Comments on “HECM vs HELOC Loan Comparison: Which is Best for You?”

|